SMM reported on July 16:

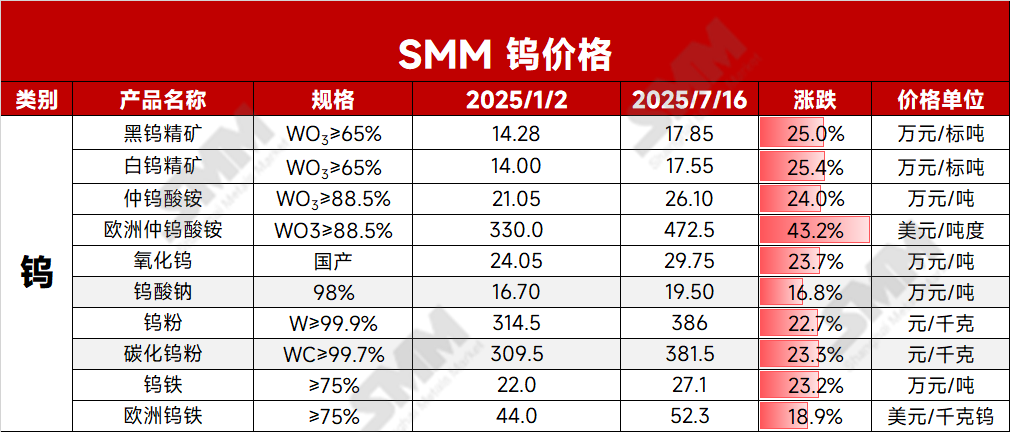

As July began, the tungsten market was once again driven by ore supply tightness, with prices climbing upwards. The circulation of tungsten concentrate in the market was tight, making it difficult for downstream players to restock. The transaction price center of spot orders rose steadily. As of today, SMM's 65% black tungsten concentrate closed at 178,500 yuan/mt, up about 25% from the beginning of the year, while 65% white tungsten concentrate closed at 177,500 yuan/mt, up 25.4% from the beginning of the year. Driven by the rapid rise in upstream ore prices, downstream ammonium paratungstate (APT) and tungsten powder products also entered an upward channel. As of today, SMM's APT closed at 261,000 yuan/mt, up 24% from the beginning of the year, and tungsten carbide powder closed at 376.5 yuan/kg, up 23.3% from the beginning of the year. The tungsten market has initiated a high-price transmission from upstream to downstream.

Long-term contracts:

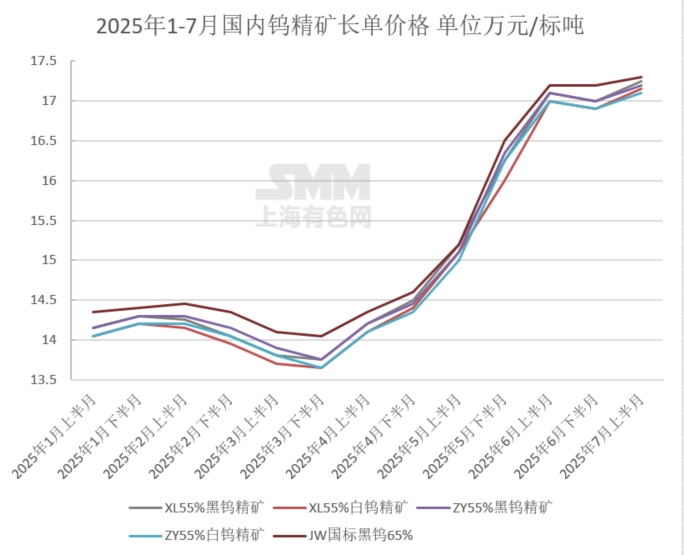

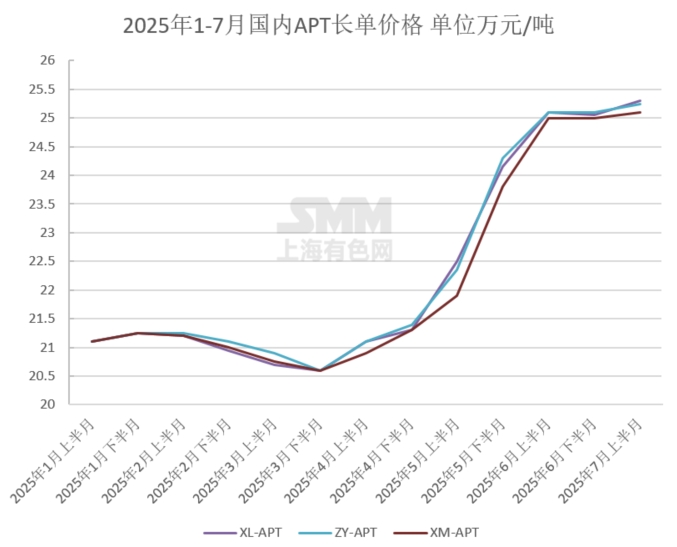

In the first half of July, long-term contracts for domestic mainstream tungsten enterprises in the first half of the month were all in an upward adjustment state. Among them, ore prices were adjusted upwards by 1,000-2,500 yuan/mt compared to the second half of June. The upward adjustment of long-term contract purchase prices for ore by mainstream tungsten enterprises also, to a certain extent, reflected the tightness of tungsten ore, driving market bullish sentiment to heat up.

Tungsten ore supply side:

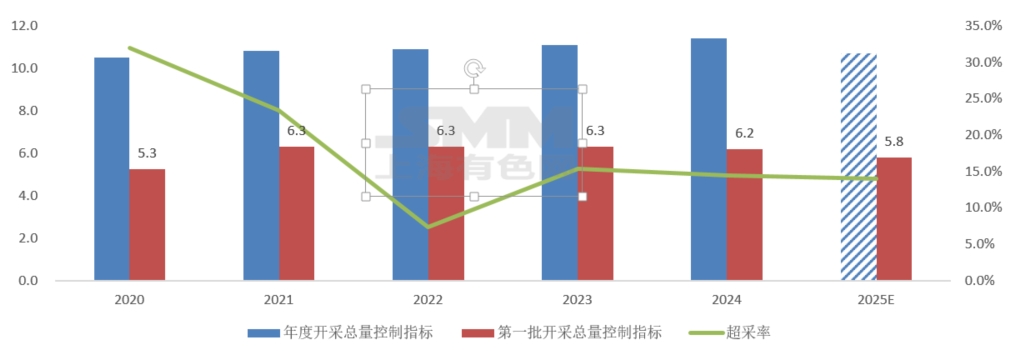

The newly revised "Mineral Resources Law of the People's Republic of China" officially came into effect on July 1 this year. The new law lists tungsten as a strategic mineral resource and implements a protective mining system. In addition, the new law requires mining right holders to carry out ecological restoration of mining areas in accordance with approved ecological restoration plans, and clarifies that the costs of ecological restoration of mining areas by enterprises should be included in production costs. This has increased the environmental protection costs for tungsten ore mining enterprises. Some small and medium-sized mines in Jiangxi and Hunan provinces that failed to meet environmental protection standards or had excessively high transformation costs have halted production or cut production, leading to a rise in market supply concerns. With the tightening of spot circulation in the market and driven by downstream bullish sentiment, the willingness to restock has increased, driving up the transaction price center.

In addition, most large tungsten enterprises adopt an integrated model of mining-smelting-deep processing, with relatively concentrated tungsten concentrate ownership. However, most of the concentrate is used for self-consumption. Under the trend of tightening tungsten ore resources, the external purchase demand of large enterprises has increased, stimulating the upward movement of ore prices.

Downstream demand: In July, traditional manufacturing industries such as domestic infrastructure, mechanical processing, and metal cutting generally entered an off-season. Coupled with the high prices in the tungsten raw material market suppressing demand, the industry's demand for tungsten products and other items has declined. Some cemented carbide enterprises have reported a MoM decrease of about 10%-20% in orders for tungsten products in the CNC blade, milling cutter, and electronic manufacturing industries.

Demand in the military sector is improving. Tungsten plays an important role in military equipment due to its excellent properties and is widely used in ammunition preparation, weaponry, aerospace parts, and tungsten steel armor. According to the 2025 central and local fiscal budget draft report, China's national defense expenditure in 2025 will be 1.784665 trillion yuan, an increase of 7.2%. This marks the third consecutive year since 2023 that China's defense expenditure has maintained a consistent growth rate of 7.2%. According to a report released by the Stockholm International Peace Research Institute (SIPRI) on April 28, 2025, global military spending reached US$2.72 trillion in 2024, a 9.4% increase from 2023, marking the largest YoY growth since the end of the Cold War. The growth in military demand has been beneficial for tungsten demand.

Overseas Tungsten Market: In July, the overseas tungsten market maintained an upward trend. Following China's implementation of export controls on ammonium paratungstate (APT) and tungsten carbide in February this year, the overseas tungsten market has experienced tighter supply. As of today, European ferrotungsten is priced at US$52-52.6/kg of tungsten (equivalent to RMB 260,700-263,000/mtu), and European APT is priced at US$460-485/mtu (equivalent to RMB 291,500-307,400/mt), creating a significant price spread with the domestic market.

In the short term, the main driving factors behind the current upward trend in the tungsten market remain the restrictions on mining quotas, ore supply tightness at the upstream level, and the rigid demand from emerging sectors such as military industry at the downstream level. Currently, upstream prices for tungsten concentrate and other products are consolidating at high levels, while the industry inversion at the downstream APT and powder end has widened. Without significant growth in end-use demand, it is difficult for the prices of these intermediate tungsten products to rise rapidly. If downstream powder production cuts occur subsequently, it will also curb the upward momentum of upstream raw material prices. In the short term, back-and-forth negotiations between upstream and downstream will dominate the tungsten market, with prices consolidating at high levels. In the medium and long term, the tungsten market may be constrained by the issue of tight ore resources for an extended period. This has also led to downstream processing enterprises without ore resources bearing higher raw material costs for a long time, resulting in industry orders flowing back to top-tier enterprises and an increase in industrial concentration. Additionally, the slowdown in growth in traditional demand sectors has also compelled the industry to switch towards orders in emerging sectors and the military industry.

》Check SMM's tungsten and molybdenum product quotes, data, and market analysis

》Click to view SMM's molybdenum spot quotes

》Subscribe to view SMM's historical price trends for metal spot cargoes